By Ryan Windt | Head of Growth Marketing | Updated June 2026

When a business tells a cyber underwriter “we follow NIST,” that sentence does almost nothing on its own. Underwriters do not price policies on framework names. They price on the specific controls a framework produces and on whether you can prove those controls are operating. NIST CSF 2.0 is the most widely referenced cybersecurity framework in the United States, and understanding how its structure connects to the questions on a cyber insurance application is one of the more practical things a security or finance leader can do before renewal.

This post walks through what changed in the 2.0 release, how each of the six functions maps to underwriting expectations, and where the framework helps or hurts your coverage position.

What NIST CSF 2.0 Actually Changed

The National Institute of Standards and Technology released CSF 2.0 in February 2024, the first major revision since the original 2014 framework. Version 2.0 replaced version 1.1, an incremental update released in 2018.

Two changes matter most for insurance buyers.

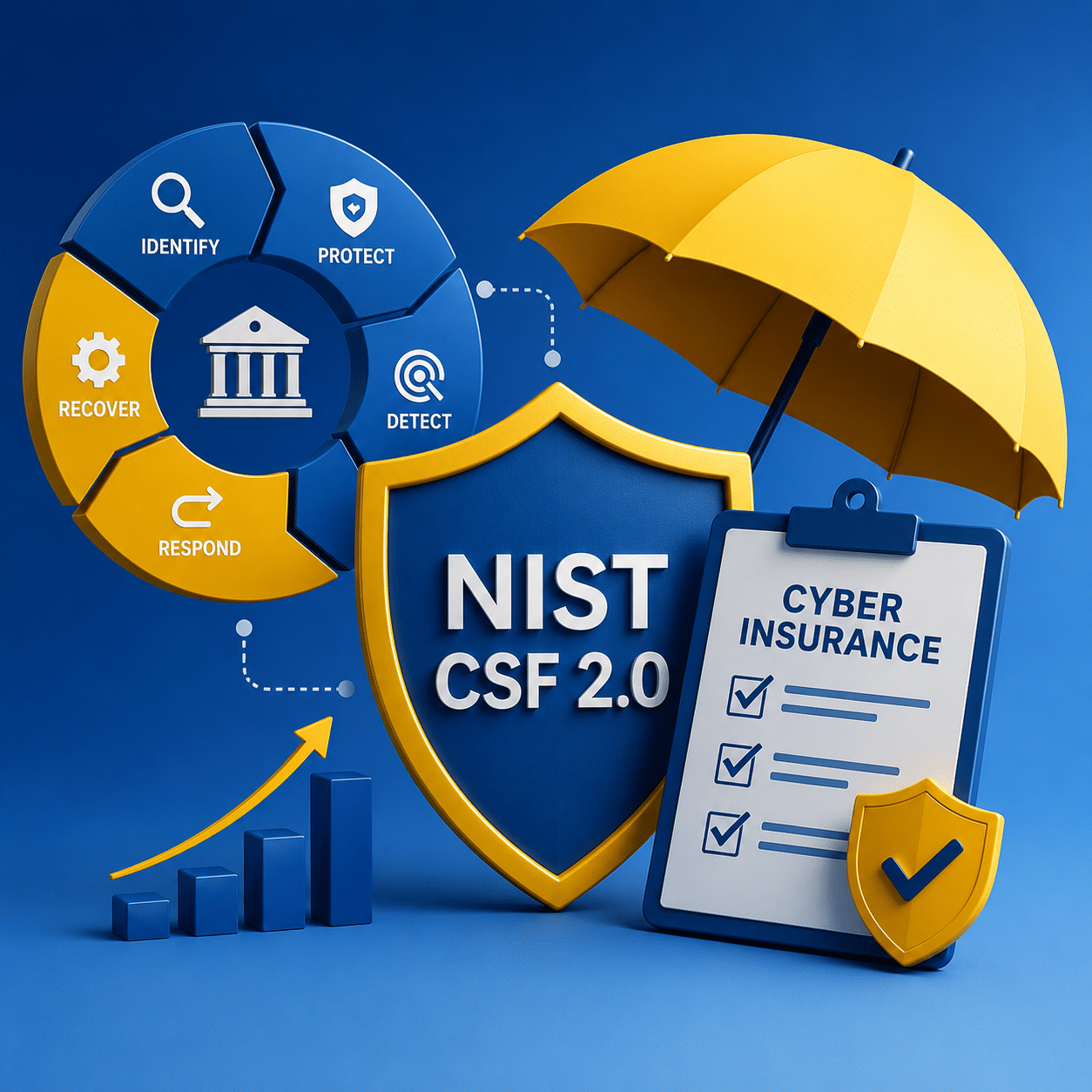

First, a sixth function. The original framework had five: Identify, Protect, Detect, Respond, and Recover. CSF 2.0 adds Govern as a sixth core function, establishing governance as a top-level concern alongside the original five. Governance was present in earlier versions, but elevating it signals that risk ownership, policy, and board-level accountability are now treated as foundational rather than supporting activities.

Second, expanded scope. NIST changed the framework’s title to signal that it now applies to every organization, not just critical infrastructure, including universities, hospitals, manufacturers, and financial institutions. That matters because the small and midsize businesses buying most cyber policies were never the framework’s original audience. Now they are squarely in scope.

Structurally, CSF 2.0 organizes cybersecurity outcomes into six functions, 22 categories, and 106 subcategories. It remains a voluntary framework focused on outcomes rather than prescriptive actions.

The framework describes what should be true (users are authenticated, assets are inventoried) without dictating how you achieve it. That flexibility is why it maps cleanly onto insurance: underwriters care about outcomes too.

The Six Functions, Mapped to Underwriting

Every cyber insurance application is, in effect, a control survey. Here is how the CSF 2.0 functions line up against what carriers actually ask.

| CSF 2.0 Function | What It Covers | What Underwriters Ask About |

|---|---|---|

| Govern | Risk strategy, roles, policy, oversight | Who owns cyber risk, incident response plan, written policies |

| Identify | Asset and data inventory, risk assessment | Asset inventory, data classification, third-party exposure |

| Protect | Access control, training, data security | MFA, privileged access, encryption, security awareness training |

| Detect | Monitoring and anomaly detection | EDR/MDR, logging, continuous monitoring |

| Respond | Incident handling and communication | Tested incident response plan, breach notification process |

| Recover | Restoration and resilience | Immutable backups, tested recovery, business continuity |

Govern

The newest function maps to questions underwriters increasingly lead with: does someone own cyber risk at your organization, do you have written security policies, and is there an incident response plan. A business that can name a risk owner and produce current policies presents as mature. One that cannot raises a flag before the technical controls are even reviewed.

Identify

Carriers want to know what you are protecting. Asset inventories and data classification feed directly into how a carrier estimates your exposure and sets sublimits. This function also covers supply chain and third-party risk, which has become a central underwriting concern after a series of vendor-driven breaches.

Protect

This is where most underwriting weight sits. Multi-factor authentication, privileged access management, encryption, and security awareness training are the controls carriers treat as near-mandatory. Missing MFA on email or remote access is one of the most common reasons an application stalls or gets declined.

Detect

Endpoint detection and response, logging, and continuous monitoring tell a carrier you can catch an intrusion before it becomes a claim. Carriers increasingly distinguish between basic antivirus and managed detection, and price accordingly.

Respond

A written, tested incident response plan is the difference between a contained event and a sprawling one. Underwriters ask whether the plan exists and whether it has been exercised, because a tested plan shortens dwell time and reduces loss severity.

Recover

Immutable, tested backups are the single strongest defense against a ransom demand turning into a payment. This function maps to the recovery questions that determine how a carrier views your ransomware exposure.

Where the Framework Helps Your Coverage Position

Citing NIST CSF 2.0 is not a substitute for controls, but mapping your program to it produces three real advantages at renewal.

It gives you a common language. Underwriters and brokers recognize the six functions, so describing your program in those terms makes your submission easier to evaluate and harder to misread.

It surfaces gaps before the carrier does. Working through 22 categories forces you to confront the control you have been meaning to implement. Finding the gap yourself, with a remediation date attached, is far better than having a carrier find it for you.

It supports the governance story. The Govern function gives finance and security leaders a structure for demonstrating board-level ownership, which is exactly what carriers want to see from larger or higher-limit applicants.

A framework does not lower your premium. Demonstrable controls mapped to that framework do.

Where It Does Not Help

NIST CSF 2.0 is voluntary and outcome-based, which means it does not tell you the specific configuration a carrier expects. Two businesses can both claim CSF alignment and present very different real-world risk. Underwriters know this, which is why the application drills into specifics: not “do you follow Protect” but “is MFA enforced on all remote access and email.”

The framework also says nothing about insurance terms themselves. It will not tell you whether your policy excludes a given loss, what your sublimits are, or how your retroactive date works. Those live in the policy, not the framework.

How This Maps to a SeedPod Submission

When we package a submission, we are effectively translating your security program into the carrier’s language. A business that has organized its controls around CSF 2.0 makes that translation faster and produces a cleaner story across multiple markets. Because we access several carriers rather than underwriting ourselves, a well-documented control program lets us position the same submission to the markets most likely to reward it.

Frequently Asked Questions

Is NIST CSF 2.0 required for cyber insurance?

No. The framework is voluntary, and no carrier requires CSF alignment by name. Carriers require specific controls, many of which the framework also recommends.

Does aligning to NIST CSF 2.0 lower my premium?

Not directly. Premiums respond to demonstrable controls and loss history. Mapping to the framework helps you implement and document those controls, which is what affects pricing.

What is the difference between CSF 1.1 and 2.0 for insurance buyers?

The most relevant change is the new Govern function, which elevates risk ownership and policy, and the expanded scope that now explicitly covers small and midsize businesses.

How does NIST CSF 2.0 relate to SOC 2 or PCI DSS?

They serve different purposes. CSF 2.0 is a broad risk framework, SOC 2 is an attestation for service organizations, and PCI DSS governs payment card data. Many controls overlap, and a single control program can support all three.

Do I need to implement all 106 subcategories?

No. The framework is meant to be tailored. You prioritize the outcomes that match your risk, which is also how you should approach the controls on a cyber application.

Related Resources

- Security Controls and Cyber Insurance

- What Underwriters Look For on a Cyber Insurance Application

- The Minimum Controls Checklist for SMBs and MSPs

- MFA Implementation Guide for Cyber Insurance

- Privileged Access Management and Cyber Insurance

- Immutable Backups and Cyber Insurance

- Incident Response Plan Template for SMBs and MSPs

- SOC 2 and Cyber Insurance

Mapping your controls to a framework is the easy part. Getting those controls in front of the right markets is where a broker earns their keep. Talk to our team about how your security program translates into coverage.